Tech-enabled platform that assists organizations to identify, understand, control, remediate and monitor compliance posture effectively and mitigate the non-compliance risks.

Get in touch with us discuss the needs and requirements of your project.

Compliance Management Software is equipped with an extensive compliance library, ensuring comprehensive coverage across industries.

Compliance Management System operates on a workflow-based mechanism, enabling configurable escalation processes up to four levels.

CMS is highly adaptable and can be customized to suit the specific needs of each client. It can be integrated with existing systems such as ERP and single sign-on..

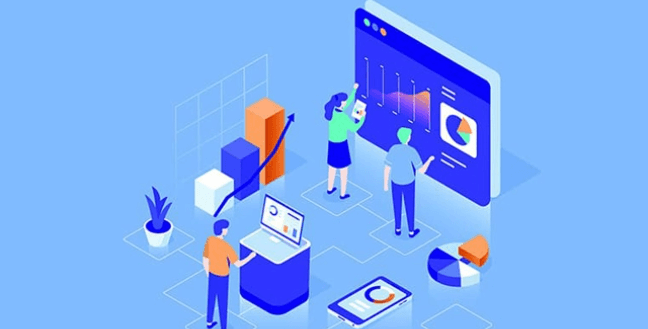

One of the system's key benefits is its ability to offer real-time insights into compliance status using trends, heatmaps, and dashboards.

User-friendly dashboards and reporting features provide a holistic view of compliance posture, making it a comprehensive compliance solution..

Alerts and notifications of the compliance solution ensure that no compliance requirement is overlooked by providing timely reminders.

Applicable compliances based on different parameters

Compliance updates on a real-time basis

Compliance mapping and controls

Compliance workbench with power tools

Value added compliance services

Compliance module covers all end-to-end compliances, including regulatory, corporate, tax, internal, and all other statutory requirements.

Notices module enables you to track notices received from statutory authorities by sending timely reminders and also serves as a repository.

Registration and Licenses module helps you keep track of the renewal dates for your recurring registrations, patents, and licenses (S & E, CLRA, etc.).

Board Meeting module helps you track all pre- and post-board meeting compliances, including the agenda, attendance, minutes of the meeting, notifications, and alerts.

Event-based module helps you track all compliance requirements applicable to a given event. Customized checklists can be added, triggered whenever an event occurs.

Risk Register module helps you track various types of risks within a company, enabling the recording and registration of these risks in a single window.

Litigation module helps you effectively manage legal matters related to compliance by tracking ongoing cases and related documents.

Contract Management module provides a centralized platform to oversee contract compliance, effortlessly monitoring milestones, renewals, and obligations.

Declaration module enables to seek declarations from the functional heads on the departmental-level compliance posture of the company.

Liaison module assists to draft and track the renewal date of all the clearances required for a project.

Bank Guarantee module helps you keep track of renewal activity for your Bank Guarantees, enabling the drafting and monitoring of approaching renewal dates.

RPT module helps in tracking any transaction, whether direct or indirect, between related parties that involves the transfer of resources, services, or obligations.

Corporate Documents module serves as a document repository for all your important documents, including customer contracts, NOC, NDA, etc.

Assessment & Survey module is used to manage internal service or training assessments that the company wishes to conduct, as well as for surveys."

Complexity of managing organization compliances across multiple legal entities/ locations/ geographies and business functions. Dynamic regulatory requirements make the process more complex, Email/excel/file share mechanisms are not collaborative and adequate andAudits or Regulatory Notices require immediate retrieval of evidences. Increased risk to Directors/CXOs/Promoters and Organization’s Brand.

Download the Case studyJoin our passionate team of missionary people with a visionary mindset.

Click on a questions to expand and reveal the answer!

RICAGO provides Governance, Risk, and Compliance (GRC) solutions that help enterprises manage regulatory, contractual, and internal compliance through a centralized and automated platform.

RICAGO offers solutions for regulatory compliance, labour law compliance, contract obligation management, GST compliance, and internal policy compliance, helping organizations stay audit-ready.

Yes. RICAGO works with startups, small businesses, mid-sized companies, and large enterprises, offering scalable compliance solutions based on organizational size and complexity.

RICAGO is used across industries such as BFSI, IT/ITeS, healthcare, energy & utilities, food, retail, high-tech, and manufacturing.

RICAGO helps enterprises by automating compliance tracking, providing real-time dashboards, managing obligations, sending alerts, and maintaining structured audit documentation.

RICAGO pricing depends on the scope, number of compliances, locations, and services required. A free compliance consultation helps determine the right solution and pricing.

Most clients begin seeing improved compliance visibility and process efficiency within a few weeks of implementation.

Yes. RICAGO provides dedicated solutions for labour law compliance, including alignment with India’s new labour codes.

Yes. RICAGO offers a Contract Obligation Management System (COMS) to track and manage contractual commitments and compliance obligations.

RICAGO is headquartered in Bengaluru, India.

You can contact RICAGO through the website enquiry form, WhatsApp, or a direct phone call to speak with a compliance expert.

RICAGO provides a complimentary compliance consultation to help businesses identify compliance gaps, risks, and areas for improvement.